SECURE Act Changes Retirement Planning

In 2019, there was a lot of buzz about the Setting Every Community Up for Retirement or the SECURE Act. Early on, this bill had bipartisan support, which is unusual in today’s political climate. The SECURE Act passed both chambers of Congress, and on December 20, 2019, was signed into law by President Trump. This single piece of legislation will have significant impacts on retirees and their beneficiaries. So, let’s dive deeper and discuss how the SECURE Act changes retirement planning.

Partial Elimination of the Stretch IRA

One of the most controversial components of the SECURE Act was the elimination of the Stretch IRA. Previously, if an IRA owner died and left the account to a non-spouse beneficiary, such as a child, the beneficiary would have the ability to take required minimum distributions from the inherited IRA over his or her lifetime. Stretching the distributions from the inherited IRA over the beneficiary’s lifetime had two main benefits. First, the beneficiary of an inherited IRA could minimize the annual tax burden by taking a relatively small amount as required by stretching the IRA withdrawals over their lifetime.

Typically, when taking money from an inherited traditional IRA, it’s taxed as ordinary income. By spreading the distribution over a lifetime, taxable income increases by a small amount each year. The second benefit is by only having to take relatively small withdrawals, the beneficiary can keep the inherited IRA growing in a tax-deferred or tax-free account over their lifetime. With the elimination of the stretch-ability of the inherited IRA under the SECURE Act, most beneficiaries must now withdraw the entire balance of the inherited IRA within 10 years of inheritance. For many beneficiaries, this will result in an acceleration of income taxes, and the additional income may be taxed at even higher rates.

From Congress’s point of view, a retirement account should fund the original owner’s retirement, not the retirement of the beneficiaries. This change has the potential to seriously increase the tax burden on beneficiaries of pre-tax retirement plans, such as IRAs and 401(k)s.

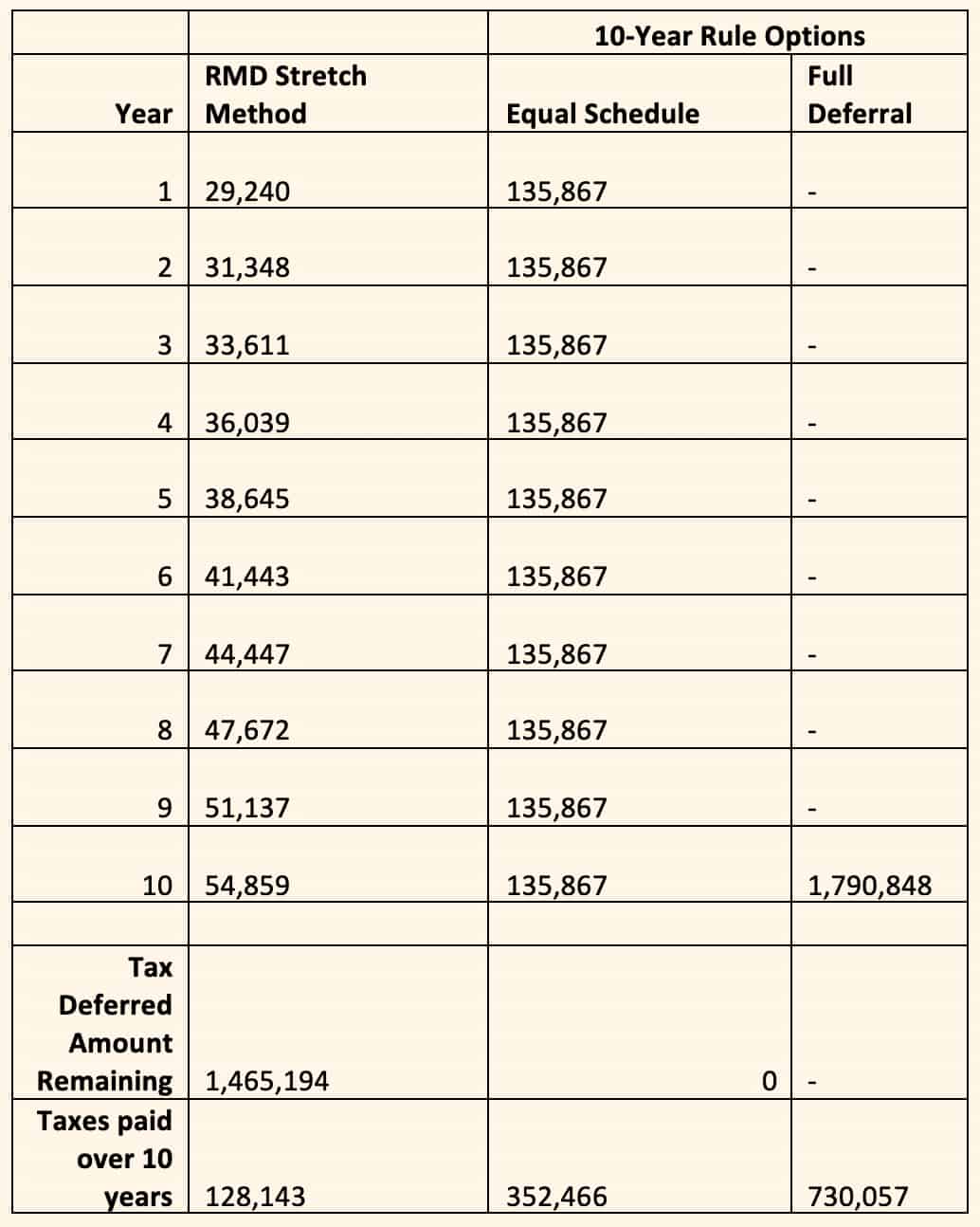

A Stretch IRA Case Study Under the SECURE Act

Assume an IRA owner dies at the age of 75, leaving a $1,000,000 IRA to his 49-year old child. The investments in the account will earn 6% per year. The required minimum distribution (RMD) for the inherited IRA owner, the first year, will be $29,240. Also, assume the beneficiary is married and has wages of $74,800. The RMD will add to this amount, increasing the federal tax liability for the first year by just over $3,500.

By the time the inherited IRA owner is 60, the RMDs have added up to just over $408,000 cumulatively. Due to the investment performance in the account, the balance is still $1,465,000. The inherited IRA owner will continue to take RMDs, stretching the account over his or her lifetime.

Under the new law, the inherited IRA owner will have 10 years to withdraw the entire inherited IRA. This change not only shortens the life of the inherited IRA to 10 years but also substantially increases the amount of taxable income to the beneficiary.

As the above shows, the inability to stretch the IRA distributions over a lifetime creates a significant increase in taxes paid over ten years. In the above example, the beneficiary pays either an additional $224,000 or $601,000 of taxes. The beneficiary also loses the tax-deferral on $1,465,000.

It’s crucial owners of tax-deferred accounts review their options to attempt to control this tax grab by the SECURE Act. This involves looking at your retirement plan, tax plan, and estate plan.

Eligible Beneficiaries

One important note is these changes don’t apply to a certain group of beneficiaries, referred to in the law as “eligible beneficiaries.” The eligible beneficiaries include the following:

- A surviving spouse;

- Disabled beneficiaries;

- Chronically ill beneficiaries;

- Beneficiaries not more than 10 years younger than the owner; and

- Minor children of the retirement account owner.

In addition, if you were the owner of an inherited IRA before January 1, 2020, you will retain the ability to take stretch IRA required minimum distributions. You may wish to consult with your financial team, including your financial advisor, CPA, and estate planning attorney, on how the SECURE Act may impact your estate plans.

Required Minimum Distributions

Things aren’t all bad for retirement plan owners, however. Another example of how the SECURE Act changes retirement planning has to do with required minimum distributions for owners of accounts like IRAs and 401(k)s. Previously RMDs began at the age of 70 ½, meaning a withdrawal must be taken from the account once the owner reached this age. The SECURE Act pushes the RMD age back to 72, buying a little more time for retirement plan owners to delay taking a taxable withdrawal. This extra year and a half may lead to proactive tax planning techniques, such as Roth IRA conversions. It also provides an opportunity to look at the distribution plan for your retirement plan to see if you need to make any changes since you’re no longer required to take an RMD.

However, if you turned 70 ½ in 2019 or earlier, you’re unaffected by this change. This means if you became 70 ½ in 2019, you must take your first RMD by April 1, 2020. You must then take your second RMD which is for the 2020 tax year by December 31, 2020. It’s important not to miss taking the RMD as it results in a tax penalty of 50% of the RMD amount. Only those born after June 30, 1949, are eligible to delay their RMDs to age 72.

Changes to IRA Contributions

Before the SECURE Act, once an individual reached the age of 70 ½, they were no longer able to make new contributions to a traditional IRA. Beginning January 1, 2020, individuals of any age may contribute to a traditional IRA as long as the individual has compensation, which is typically income from wages or self-employment. This means only individuals that are still working or have a spouse that is working are eligible to contribute to a traditional IRA. This change presents another opportunity for retirement planning. Now you have the choice between contributing to a traditional IRA or Roth IRA even after reaching age 70 ½. In the Guided Retirement Show, Season One, episodes one and two, Dean and JoAnn discuss this. Since this is a decision that varies depending on your individual situation, we can help you determine which is best for your situation.

Qualified Charitable Distributions

The SECURE Act does not change the ability to make qualified charitable distributions (QCDs) once you are age 70 ½ or over. A QCD allows you to make a direct distribution to a charitable organization from your IRA. By making the distribution as a QCD, you don’t have to include the amount in income, which can result in tax savings. Once you reach age 70 ½, you can make QCDs of up to $100,000 per year.

The SECURE Act made an essential change to the QCD rules to prevent the ability to double-dip and receive two tax benefits for the same money. This rule is the QCD anti-abuse rule. Without this rule, you would be able to make a tax-deductible contribution to your IRA, if you had earnings, and then immediately make a qualified charitable distribution.

For example, you are 73 years old and make a traditional IRA contribution of $7,000, which reduces your taxable income. If you then make a QCD of $7,000 to your favorite charity, you don’t have to include the $7,000 in your taxable income.

The QCD anti-abuse rule requires you to reduce your allowed QCD limit for the year by the aggregate amount of any post-age 70 ½ deductible contributions to your IRA. Once the amount of your post-age 70 ½ deducted contributions meet with attempted QCDs, you will be eligible to have any excess amount treated as a QCD and not included in taxable income.

How Do QCDs Work?

Let’s look at how this works. Let’s assume you have made $10,000 of deductible contributions to your IRA after reaching age 70 ½. This year you decide to make a QCD to your favorite charity of $15,000. You are only allowed to exclude $5,000 from taxable income on your tax return for the QCD since you had $10,000 of deducted IRA contributions after age 70 ½. Your taxable income includes the $10,000 of post-age 70 ½ deductible contributions to your IRA. However, you can include the $10,000 as a charitable deduction on Schedule A of your tax return. The remaining $5,000 is still allowed as a QCD.

If you don’t make any future deductible contributions to an IRA after age 70 ½, all future QCDs will be allowed to the extent they meet the QCD rules. To continue the above example, if we assume in the following year, you make another $15,000 QCD. The entire $15,000 will be allowed as a QCD.

It’s essential if you’ve made deductible contributions after age 70½ and want to take advantage of QCDs that you have your IRA custodian send the funds directly to the charity the same as any QCD. If you take an IRA distribution then donate it to a charity, you won’t be able to eliminate that amount from your post-age 70 ½ deducted amount. And you’ll have to continue to track it until you have made attempted QCDs equal to the amount of your post-age 70 ½ deducted amount. Once these have been subtracted, then you can continue to make QCDs and receive the special tax treatment.

What About IRA Distribution Instead of a QCD?

Let’s use the same assumptions as above that you have made $10,000 of deductible contributions to your IRA after reaching age 70 ½. Instead of making a QCD this year, you decide to take an IRA distribution of $15,000. Then, you write a check to the charity for $15,000 since you won’t be able to take full advantage of the QCD. In this situation, you will have to include the $15,000 distribution in ordinary income and take a charitable deduction for the $15,000. If the following year, you decide to make a QCD of $15,000, then you are only able to exclude $5,000 from taxable income while including $10,000 in taxable income to offset the deductible contributions you made earlier. Over the two years, you include $25,000 in taxable income compared to the $10,000 included in taxable income under the first scenario.

An important part of the retirement planning process after the SECURE Act will be to weigh the long-term tax implications of making deductible IRA contributions against the tax benefit of QCDs. We can help you run the numbers to decide what is most beneficial for you.

The exception to the 10% Early Withdrawal Penalty for Adoption and Childbirth

The SECURE Act adds a new provision allowing a retirement plan owner to take up to a $5,000 penalty-free withdrawal for qualified adoption or qualified childbirth-related expenses. The withdrawal is still included in taxable income but is exempt from the 10% early withdrawal penalty.

You may take a qualifying distribution at any point during the one year beginning on either the date of birth or the date on which the adoption of an individual under the age of 18 is finalized. The $5,000 is on a “per birth or adoption” basis. It is also on an individual basis. This means if both parents have qualified retirement accounts, they may both take a distribution of $5,000 to total $10,000 without any penalties. The parent is also able to repay the amount withdrawn as a rollover contribution to an eligible defined contribution plan or IRA if funds are available in the future.

We can help you determine the impact of using your retirement funds to pay for the birth or adoption of your child.

Annuity-Related Changes to Employer Retirement Plans

With the advent of the SECURE Act, we’ll likely see more annuities make their way into the 401(k) space. Previously, the plan’s fiduciary would conduct extensive due diligence when selecting a lifetime income provider such as an annuity provider for a retirement plan’s participants to utilize. Now, there is liability protection for the plan’s fiduciary in the event the annuity provider is unable to pay future obligations to plan participants.

Another change is these annuities are now portable as the SECURE Act creates a new distributable event that applies just to annuities when they are no longer allowed as an investment option within a retirement plan. In this situation, you would be able to distribute the plan annuity, in-kind. If you leave your job, then you are also able to roll over the 401(k) annuity you had with your former employer to another 401(k) or IRA. Previously, you may have been forced to surrender the annuity, which may have caused you to be forced to pay surrender charges and fees.

These two changes are a big win for annuity providers who lobbied for these provisions under the SECURE Act. It remains to be seen how this will work out for savers in retirement plans. We can help you determine if the purchase of an annuity in your qualified retirement plan improves the success of your retirement plan.

Allow Long-term Part-time Employees to Participate in 401(k) Plans

Currently, employers are generally able to exclude part-time employees (i.e., employees who work less than 1,000 hours per year) when providing certain types of retirement plans—like a 401(k) plan—to their employees. This leaves many part-time workers ineligible to participate in a retirement plan and can be harmful to them in preparing for retirement.

Starting in 2021, the SECURE Act implements new rules which will require most employers maintaining a 401(k) plan to have a dual eligibility requirement under which an employee must complete either a one-year-of-service requirement with the 1,000-hour rule or three consecutive years of service where the employee completes at least 500 hours of service per year. For employees who are eligible solely because of the new 500-hour rule, the employer can exclude those employees from testing under the nondiscrimination and coverage rules, and from the application of the top-heavy rules.

These changes apply to plan years beginning in 2021. However, the SECURE Act does not require an employer to start counting a 500-hour year as a 500-hour year for this new rule until 2021. This means the earliest an employee would be eligible to participate in a 401(k) plan as a result of this change will be in 2024.

This change creates an opportunity for retirement planning as part-time workers will have an increased ability to participate in employer retirement plans. We can help you decide if saving to the 401(k) is the right choice for you.

529 Plan Changes

The SECURE Act also made some changes to rules for 529 plans. One of the changes is distributions for “Qualified Education Loan Repayments” are treated as a qualified higher education expense. This means the ability to use 529 funds to pay down up to $10,000 in student debt over the student’s lifetime. If there’s money left in the 529 plan, each sibling of the 529 beneficiary may have $10,000 toward student debt payments on their behalf as well.

Another change under the SECURE Act is the ability to use the 529 plan to pay for certain apprenticeship programs. The SECURE Act provides qualified higher education expenses include expenses for apprenticeship programs that include fees, books, supplies, and required equipment, provided the program is appropriately registered and certified with the Department of Labor.

Although some may consider this to be a non-retirement provision, paying off student debt may allow you to begin saving sooner for retirement.

What Do I Need to Do Now

It’s clear that in no small way, the SECURE Act changes retirement planning, for better or worse. We focused on changes in the SECURE Act most likely to impact our clients but haven’t discussed all the changes. Any time major legislation passes that can affect your retirement plan, it’s an excellent opportunity to revisit your plan and measure the potential changes it may have on your goals. The SECURE Act impacts the four pillars of wealth management – investment, tax, estate, and insurance. Now is the time to determine what changes you need to make.

Does your estate plan still work as desired? Are you overpaying your taxes? Or are there steps you can take to minimize the taxes both you and your beneficiaries will pay? How can insurance enhance your plan? If you’re working with a Modern Wealth Management advisor, make sure to bring this up at your next meeting. You can also contact us at (913) 393-1000. If you’re not working with us and would like to speak with an advisor, please fill out the form below, and we’ll get in touch.

Let's Get in Touch

Investment advisory services offered through Modern Wealth Management, Inc., an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.